Ending your relationship with debt is a journey that takes time, planning, and ultimately, a little bit of math. We created a debt payoff worksheet to help you gain a good understanding of your income, expenses, and how much money you can put toward your debt every month. Our worksheet enables you to crunch the numbers to choose a strategy that is right for your circumstances.

Income – Expenses = How Much You Can Put Toward Your Debt

Before you can make a debt payoff plan, make sure you can answer a few budget questions:

- How much is your total monthly income?

- How much are your total monthly expenses?

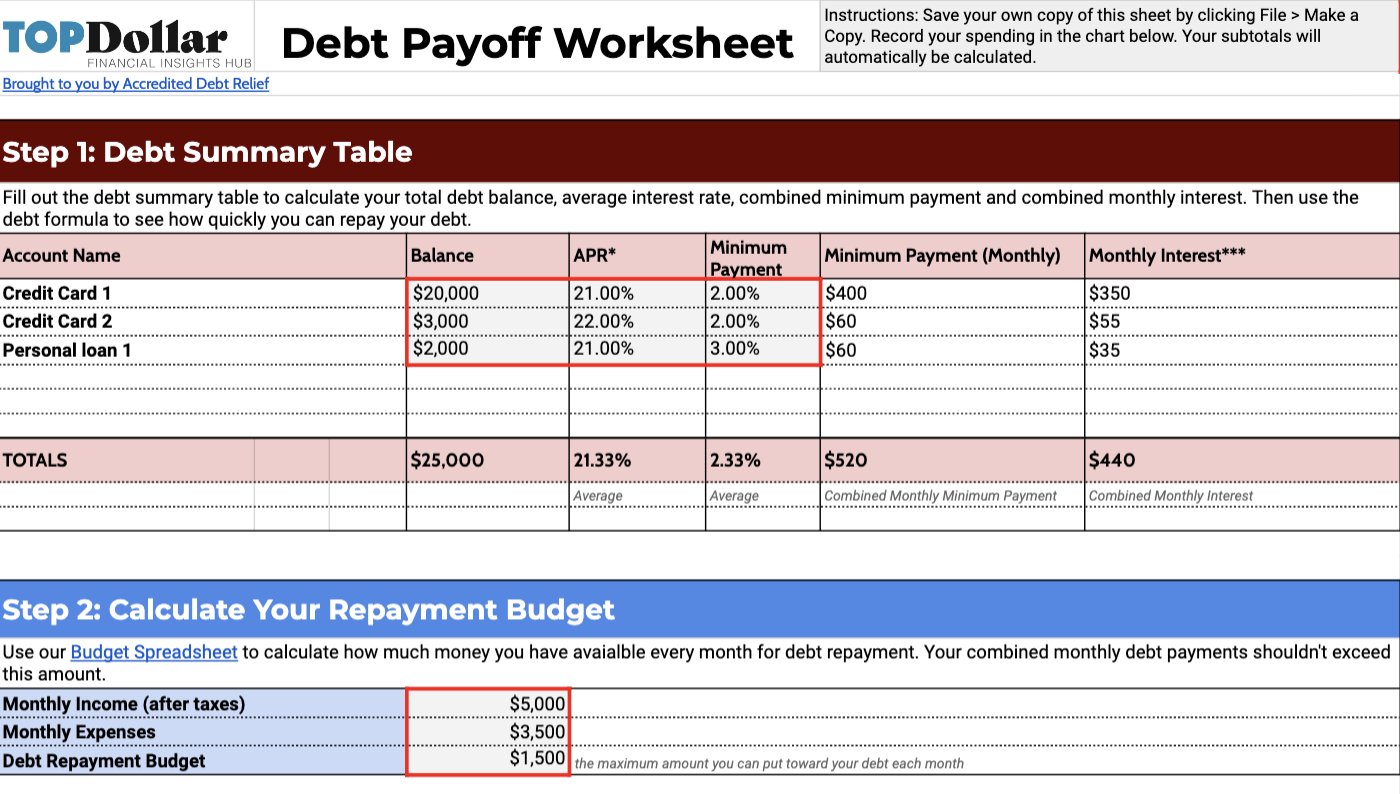

Our free budget spreadsheet can help you add up your monthly expenses, both consistent and not consistent.

Top Dollar’s Free Debt Payoff Worksheet

Download your copy of the worksheet to estimate how much money to put toward your debt each month and how long it will take to pay off.

It will help you complete the ‘get out of debt’ formula:

Pay off $__ Debt for $__ a Month in __ Months

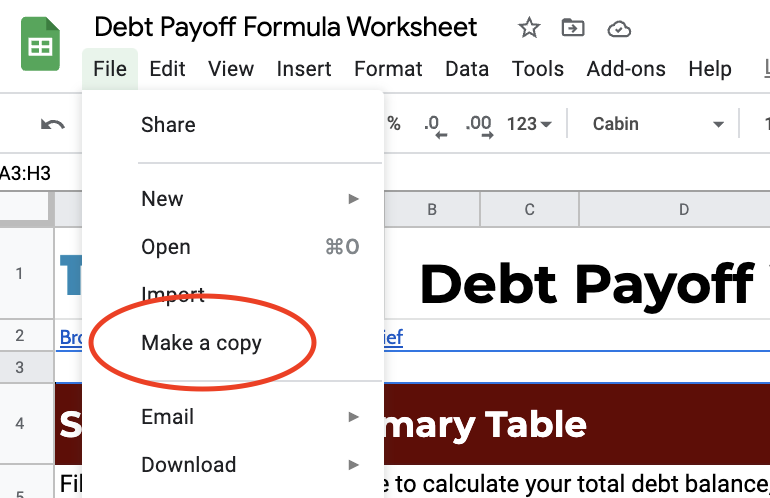

Our copy is locked for editing, but you can save your version to edit as you please. Simply click “File” and “Make a copy” in the upper left-hand corner to save.

How Long Will it Take Me To Pay Off My Debt?

The amount of time it takes to pay off your debt depends on both your interest rates and how much you owe, as well as the repayment strategy you take.

Making minimum payments is usually the slowest way to pay off your debt. If your debt has a high interest rate (typically anything over 10%), it will take longer and cost you more money. When you make minimum payments, most of your money is going towards interest instead of the principal. The minimum payment will decrease as the principal balance goes down, lengthening your repayment period.

On the other hand, making regular monthly payments of the same amount helps speed up the process. Other debt strategies can also help speed up repayment.

Choosing a Debt Payoff Strategy

The debt payoff strategy you choose depends on the type and number of debts you have. Options usually include some combination of the following:

- Making Minimum Payments

- Making Regular Payments Greater than Monthly Minimums

- Making Larger One Time Payments in Addition to Monthly Minimums

- Negotiating For a Lower Interest Rate

- The Snowball Method: Paying off by Balance, Small to Large

- The Avalanche Method: Paying off by Interest Rate, High to Low

- Debt Consolidation for Multiple Debts

Stay Out of Debt for Good

Following a debt payoff plan helps with the aftermath of debt and draws on skills that could help you stay out of debt in the future. For example: creating a budget and following a payoff plan helps you better understand where your money is going each month.

You can take that progress a step further by addressing other concerns like impulse buys and making changes to spending habits that led to your debt.

When Debt Payoff Strategies Aren’t Enough

Sometimes, despite our best efforts, debt gets out of control. If your debt is too high and these strategies are not helping, it may be time to consider debt consolidation. It’s an alternative to making minimum payments and bankruptcy that helps lessen the burden of debt.

Speak with a Consolidation Specialist to see if debt consolidation is a good option for you.