If you have short and long-term financial objectives, try running a SWOT analysis on your finances to pinpoint your priorities and highlight where you could make improvements. A SWOT analysis is a strategic matrix developed to help businesses identify things standing between them and their goals. It’s also a great way to distill down your priorities when making important decisions. Although originally intended for organizations, the exercise can be useful for all types of goal setting and analysis.

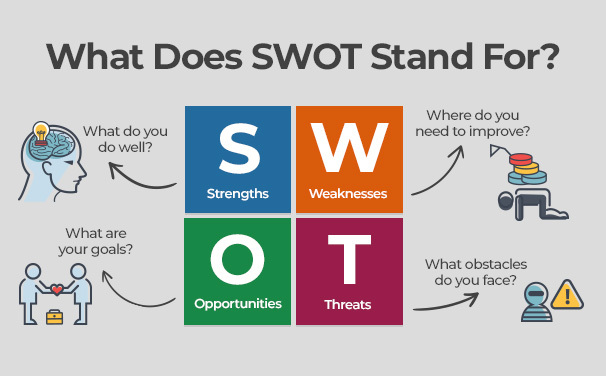

SWOT is an acronym that stands for: Strengths, Weaknesses, Opportunities and Threats. These elements are all important variables that can influence your ability to achieve long and short-term objectives. They can be helpful if you feel like your growth has stagnated or you’ve been stuck in one phase of your development for too long.

Internal vs. External Variables

Recognizing when a variable is external or internal is a critical factor in any SWOT analysis. For example, anything listed under strengths and weaknesses is considered internal because these are things over which you have some kind of control. In contrast, opportunities and threats are external factors that you can’t necessarily control. Identifying external variables helps you seek out positive opportunities and avoid harmful threats.

Run Your Own SWOT Analysis: Step by Step

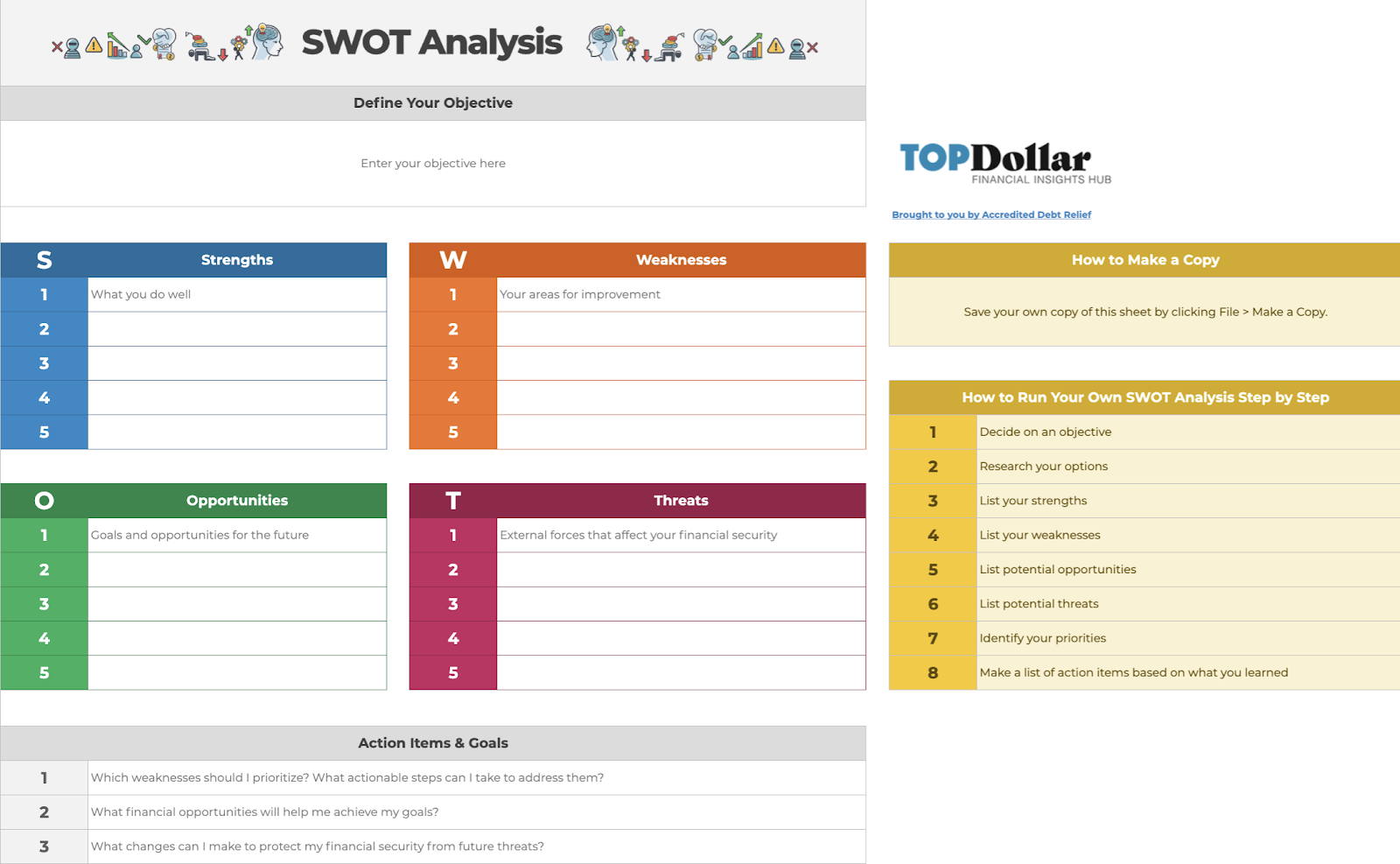

In a traditional SWOT analysis, you would begin by choosing an objective that analyzes a narrow part of your business. For financial analysis, you may want to focus on one area like, spending, investing, or saving. Alternatively, you may choose to do a more general evaluation of your financial plan.

Both approaches have merit. However, if you decide to run a general analysis and find that each list is growing quite long, you might want to reevaluate your approach. See if you can break your analysis down into manageable sections to focus thoroughly on important details.

SWOT Analysis Step by Step

- Decide on an objective

- Research your options

- List your strengths

- List your weaknesses

- List potential opportunities

- List potential threats

- Identify your priorities

- Make a list of action items based on what you learned

Tips for Filling Out the SWOT Matrix

When you fill out the matrix, try to do it quickly and without overthinking each response. Write quickly and without censoring yourself. If at any point you feel “writer’s block,” try a stream of consciousness approach, allowing your thoughts to flow freely and continuously. After you have gotten out those ideas, you can back and organize those thoughts into a list of bullet points for each category.

Once you’ve made a comprehensive list for each quadrant, review and circle 1 or 2 of the most important items from each section, you may find that one category has a longer list than the others. That can be illuminating in and of itself. However, suppose your list for each category is bursting. In that case, you might benefit from narrowing the objective and repeating the exercise a few times for different aspects of your financial planning.

Whatever method you choose, make sure you have a good understanding of what belongs in each category. You should assess your strengths and weaknesses in a unique way to you and your finances, so don’t hesitate to customize your list. If something comes to mind, write it down. You’ll have a chance to edit and refine the lists later.

Strengths: What You Do Well

Financial strengths might include a low debt to income ratio, a healthy savings account, or good habits like paying off your credit card every month and automating savings and investments.

Check out the list below for some other examples:

- A strong emergency fund

- Paying off credit card balance every month

- Low debt-to-income ratio

- A healthy savings account

- Automated savings each month

- Automated bill payment

- Automatically investing a portion of your income every month

- Automated retirement savings

- Finances are regularly organized

- Spending and saving are regularly monitored

Weaknesses: Your Areas for Improvement

This list should include anything that you know you could do better. You might want to include things like missing payments, high debt-to-income ratio and having no emergency fund or retirement savings.

- Losing track of your bills/payments

- The debt-to-income ratio is high

- Owing money to family or friends

- Chronically deferring student loan payments

- Organizing financial paperwork overwhelms me

- Having a hard time estimating what I can afford

- Not planning for my taxes

- Making big purchases on credit

- No emergency fund

- No retirement savings

- Employer doesn’t offer a retirement plan

- High-interest rate debt that I am paying down too slowly

- Not asking for expert help when I need it

- Income is unstable

- Impulse buying

- Expenses are too high (i.e., housing costs, bills, debt payments, medical bills, etc.)

- My debt affects my mental health

What Opportunities Should You Consider?

- Opening a retirement account

- Automate saving and investing with an app

- Redo your budget to reflect your spending habits more accurately

- Restructuring debt

- Increasing income with a new job or a freelance side hustle

- A new debt repayment strategy like snowball vs. avalanche

- A new budgeting strategy like 50/30/20

What External Forces Threaten Your Financial Security?

- Job insecurity caused by the pandemic

- Insurance is not robust enough to handle a severe medical emergency

- High-interest debt

- Cost of living increases

Example of a Completed SWOT Analysis

Choosing Your Opportunities

Ideally, your opportunities should address one or more of the weaknesses or threats that you identified. Look at each list and try to match up weaknesses and threats with a corresponding opportunity. If you have a weakness that isn’t addressed by your opportunity list, you can do some research to find an actionable solution.

Be Ready for Financial Threats

The most pressing threats will be ones that impact your financial strengths. For example, if you have regular income from only one job, losing that job could significantly impact your finances. The solution can be identified in the form of an opportunity. One opportunity might be: picking up a side hustle that allows you to make extra income that will pad your savings and give you a safety net if your primary job is terminated.

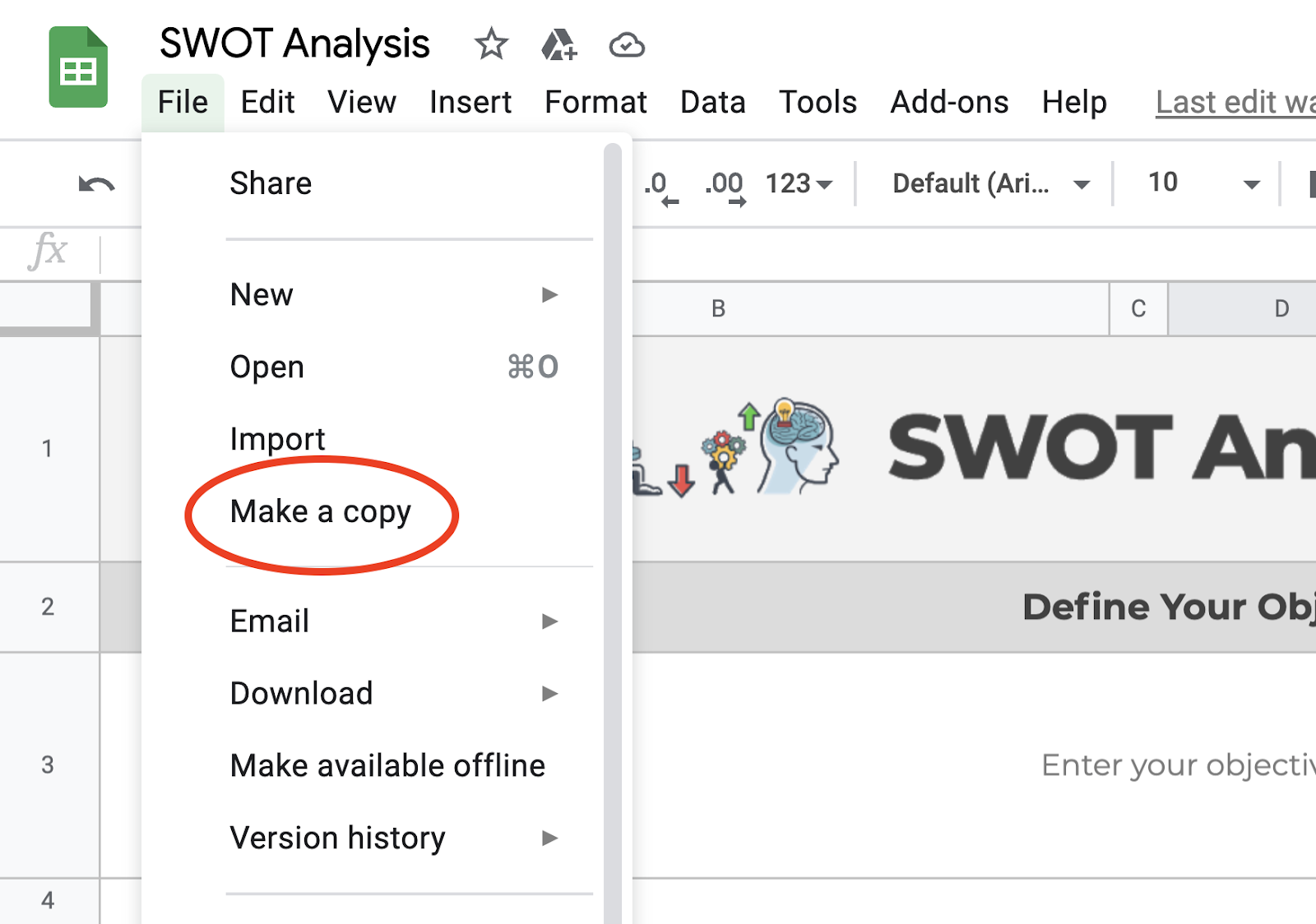

Complete Your Own Swot Analysis

Get started with our downloadable Financial SWOT Analysis worksheet in Google sheets.

Our copy is locked for editing, but you can save your own version to edit as you please.

If you have a Google account: simply click “File” and “Make a copy” in the upper left-hand corner to save.

If you don’t have a Google Account: simply click “Download” to save the spreadsheet as a PDF or Excel file.

Focus On Your Priorities

Analyzing your financial situation can be stressful, but it can also be empowering. Remember, you don’t have to tackle everything on your SWOT list right away. It’s not a good idea to focus on too many action items at once. Instead, set yourself up for success by prioritizing your list and tackling them a few at a time.

For example, if saving for an emergency fund is a top priority, break it down into a few tasks and add them to your calendar. First, determine how much you need to save and then save the amount in manageable increments over a predetermined length of time.

If your goal is to change spending habits, find small, achievable changes to get started. It’s much easier to cut things from your spending little by little than it might be to go cold turkey on take-out or your weekly coffee trips.

Equip Your Financial Toolkit

Automate any and every aspect of your finances that you can. We live in a time where there truly is an app for everything! Take advantage of these resources, even if they are initially out of your comfort zone.

Things you should be automating:

- Bills pay

- Monthly savings

- Investments

- Expense tracking

Check out this comprehensive list of apps for your financial toolkit.

Ask For Expert Help When You Need It

Analyzing your finances with a SWOT analysis and creating a list of action items to help you achieve your goals is a wonderful way to take charge of your finances. However, it’s never a substitute for objective professional advice. That is especially true if you are already doing a lot of things “right.”

If you are consistently making responsible financial decisions but still feel like you aren’t making enough progress toward big financial goals, it might be time to call in an expert. Financial advisors can help you take your investments and retirement savings to the next level.

Alternatively, if your debt is out of control, and you feel like you are stuck, a Consolidation Specialist can help you make informed decisions about your debt. Most debt consolidation options can help you pay off your debt in 12 to 48 months for less than you owe without the lingering mark of bankruptcy on your credit report. If you haven’t considered all your options and bankruptcy alternatives, you should rule them out before making a decision.

Speaking with a Consolidation Specialist at Accredited Debt Relief is free, so call today.