When you go to an ATM you probably take out twenties more than any other denomination. Twenty-dollar bills account for 23% of all currency in circulation, second only to the dollar bill (31%). While you do your best to stretch your money as far as it will go, you are fighting an invisible force that guarantees the purchasing power of $20 will decline year after year.

The Invisible Hand of Inflation

They say, “money doesn’t go as far as it used to.” The saying has been repeated by every generation since the 1940s, and the reason is simple: the invisible hand of inflation. Inflation is a gradual increase in the cost of goods and services. Over time, it causes the value of our currency to down.

A Dollar Buys 92.5% Less Than it Used To

Over the past 100 years, inflation has driven down the purchasing power of a dollar. I researched inflation rates and discovered that a dollar buys 92.5% less than it used to. The results are even more surprising when you look at what you could buy with a $20.00 bill over the past century.

The Purchasing Power of $20 Over the Past 100 Years

What Causes Inflation?

Inflation is a gradual increase in prices and a fall in the purchasing value of money. It leads to a rise in living costs over time and is a natural side effect of developed economies. It is usually driven by increases in production and demand that fall into a few categories:

- Cost-push inflation

- Demand-pull inflation

- The Housing Market

- Fiscal Policy

Cost-push-Inflation vs. Demand-pull Inflation

Cost-push inflation and demand-pull inflation have similar outcomes but affect different systems. When either occurs, the cost of goods goes up, and the purchasing power of the dollar goes down. As a result, policies are enacted to stabilize the economy.

For cost-push inflation to occur, demand for goods must be unchanging. Instead, the cost of production must go up. That can be caused by competition for resources. An increase in commodity prices like copper often goes hand in hand with cost-push inflation.

If the economy is performing well and unemployment is low, there will be more competition for qualified workers. If companies raise wages to attract talent, the cost of production goes up, and cost-push inflation occurs.

On the other hand, demand-pull inflation occurs when the consumer appetite for a product exceeds its current production. As a result, companies can raise prices on high-demand goods and use increased profits to ramp up production.

The Housing Market and Fiscal Policy

The housing market and fiscal policies enacted by the government also have an impact on inflation. If the economy is expanding and homes are in high demand, prices will rise, and the seller’s market will spike bidding wars among prospective buyers.

Likewise, when the government cuts taxes, consumers will have more disposable income to put back into the economy. The government can also stimulate the economy with infrastructure projects that create jobs. An increase in goods and services can lead to price increases that drive inflation.

During the COVID-19 pandemic, the government provided economic relief with the CARES Act, which included stimulus payments, eviction moratoriums, added unemployment benefits, and more to help keep the economy afloat during the lockdown.

During periods of economic difficulty, the government can also change the interest rate for all federally backed loans, which helps both consumers and businesses.

The Federal Reserve and Money Supply

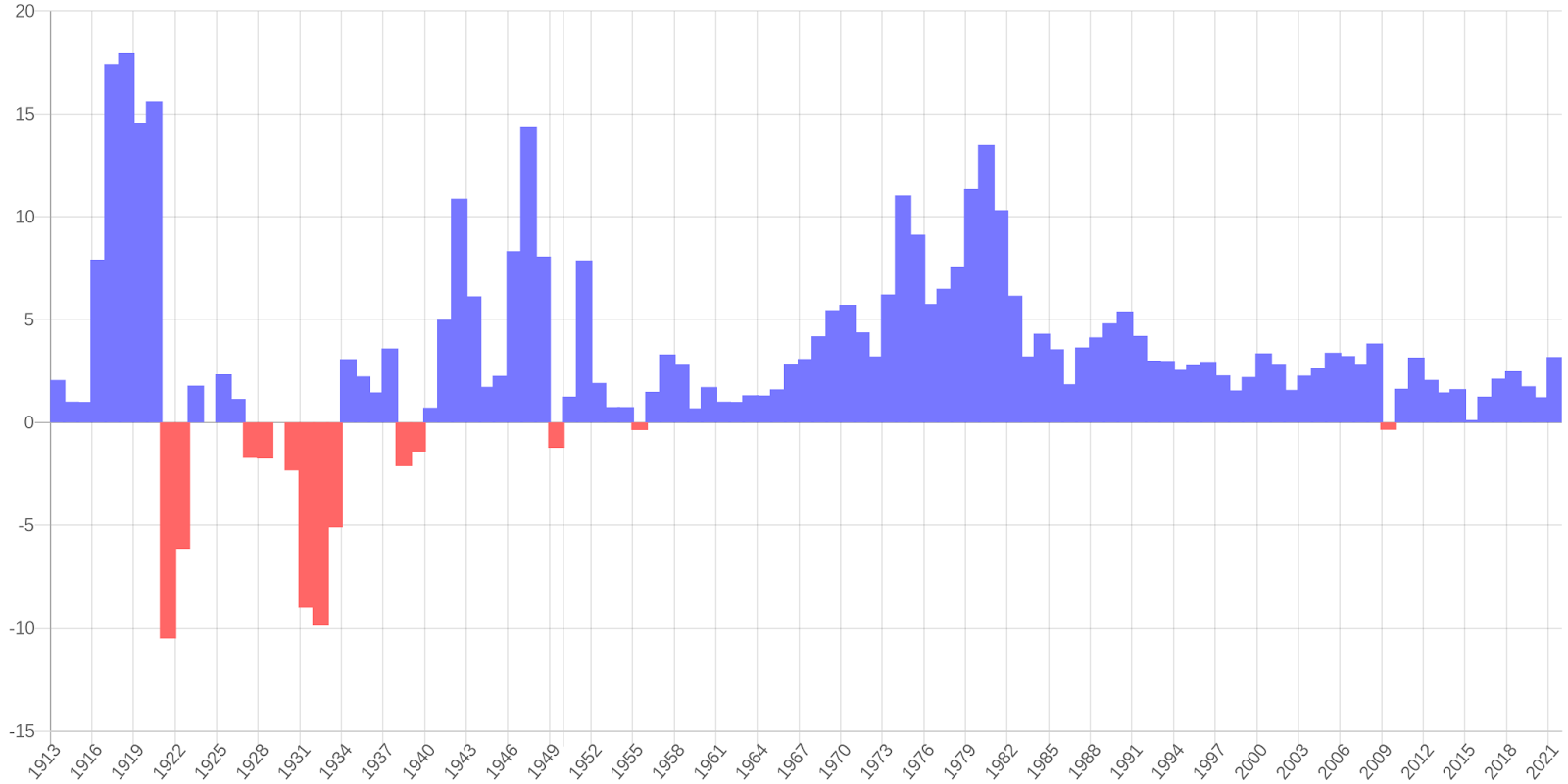

In 1913, The Federal Reserve Act granted Federal Reserve banks the ability to manage the money supply in order to ensure economic stability. They began by putting more currency into circulation. In those days a dollar was a decent amount of money, it could buy $13 worth of goods and services by today’s standards.

As more dollars came into circulation, the prices of goods and services increased while the purchasing power of the dollar fell. By 1929, the value of the Consumer Price Index (CPI) was 73% higher than in 1913.

Inflation Has Been Steadily Rising Since The Great Depression

During the great depression, from 1929 to 1933, the value of the dollar reached all-time lows. After 1933 the economy started to recover, due in large part to government policies such as the New Deal. However, those policies did not reign in inflation and may even have contributed to it’s sharp rise and demand for goods increased.

The Stabilization Act of 1942 was an anti-inflation executive order that aimed to curb inflation through wage freezes and salary caps. However, it wasn’t enough to stabilize the wartime economy and was so unpopular that it led to resignations and labor strikes. It is also seen as the biggest catalyst for the development of employee insurance plans and pension benefits which were exempt from the legislation.

Ultimately the act did little to halt inflation and backfired when it was removed. When price controls ended in the summer of 1946 the suppressed inflation that had built up during the war was unleashed.

In 1947 the inflation rate peaked at 14.36% meaning prices were 14x higher than they were in 1920. It eventually stabilized Since then, the inflation rate has ebbed and flowed since with significant peaks in 1974 and 1980, and a depression-era low in 2008.

USD Inflation since 1913

Annual Rate, the Bureau of Labor Statistics CPI

Source: In2013dollars.com

Getting More Purchasing Power Out of $20

Although inflation has stabilized since the mid-70s to an average year-over-year increase of 2.2%, it continues to worry economists. Inflation rates went up to 4.4% in the wake of the COVID-19 pandemic and economists suspect that the average could once again creep up. So what can you do to get more purchasing power out of your money in the face of this unstoppable force?

First, you need to understand what inflation means for your money. For example, if you have $100,000 in the bank and the average inflation rate increased to 3.5%, in twenty years the purchasing power of your money will be worth around $50,000. That’s a scary proposition.

Protect Yourself From Inflation

Most experts agree that you should work with the current economic system by optimizing your investments to insulate them from the effects of inflation. To begin with, keeping a significant amount of money in a bank account that is not earning you enough interest to outpace inflation, is the worst thing you can do with your capital.

Instead, you should:

- Invest in Stocks

- Invest in Real Estate

- Increase your earning potential year over year

Investing your money so that its growth outpaces the inflation rate is essential. Additionally, real estate investments are considered particularly good for beating inflation because property appreciates with the economy. Lastly, you should aim to get a raise on par with the inflation rate each year in order to ensure that your cost of living stays the same. Many employers will offer cost of living raises, but if they do not, you can invest in your education and career skills to make yourself desirable to hirer-paying employers.